February 8, 2021 | Blog

Why Late-stage Venture Funded Companies are Poised for a Potential 2021 Break Out—And How Investors Can Buy In

As the U.S. economy’s digital transformation accelerates, there’s no turning back the clock to the pre-COVID economy. Increasingly, technology and innovation are integrated into the entire economy, across all industries and sectors.

In early 2020, as in past years, the adoption of new technology and innovation increased at a steady level. COVID-19 then turned up the volume on digital transformation across industries, the country and the globe. Technology and innovation are the future—and the present. In fact, according to McKinsey, the rate at which companies have accelerated digitization is now every three to four years.

With technology and innovation increasingly leading the economy, many investors are searching for the best opportunities to capitalize on these trends. As more growth amongst these areas occurs outside of the public markets, investors are turning to the private markets, particularly the late-stage venture capital market.

These trends are aligning with the rollout of COVID-19 vaccines across America, potentially brightening the economic outlook for 2021. Investors seeking to stay ahead of the curve are seeing opportunities in the late-stage venture market.

An Emerging Opportunity

When COVID-19 and related policies forced a shutdown of businesses across the country, many of the companies that flourished were those that had the deepest digital footprints. Firms quickly pivoted to digital technologies and innovative solutions, compressing digitalization timelines to months from years.

This acceleration of technological innovation pulled addressable market penetration rates forward, driving growth. While the markets quickly rewarded stay-at-home publicly traded companies such as Zoom, Amazon and Netflix with higher valuations, the improving prospects for late-stage venture companies remained largely outside the public view.

Numerous late-stage venture-backed companies in appealing sectors—remote working, virtual learning, telemedicine, data analytics, cloud migration, cyber-security, genomics, digital therapeutics, ecommerce and last-mile delivery—may be poised to expand their market share and penetration. This is due to permanent behavioral changes that will persist beyond the COVID-19 environment. Such non-public companies have the potential to eclipse the gains of their publicly-traded counterparts as they continue scaling and appreciating in value in the private markets.

How much opportunity? $3.5 trillion in excess cash remained on market sidelines at the end of 2020.

Private Companies Staying Private Longer

Private companies are staying private longer. This is both a cause and effect of the increased capital flows into the space. Previously, companies such as Amazon were forced to access the public markets for capital at a much earlier phase in their development because they needed access to public market capital to grow. As a result, much of Amazon’s value appreciation was generated as a publicly traded company.

Increasingly, institutional cash has pulled up stakes from the public markets and moved some of that capital to the private markets. Why? Because the investment managers running these institutional vehicles are skeptical about the efficiency and upside potential of public markets and believe the opportunity for alpha generation in the less efficient private markets can be significant. Their skepticism is justified. (Alpha refers to excess returns earned on an investment above the benchmark return.)

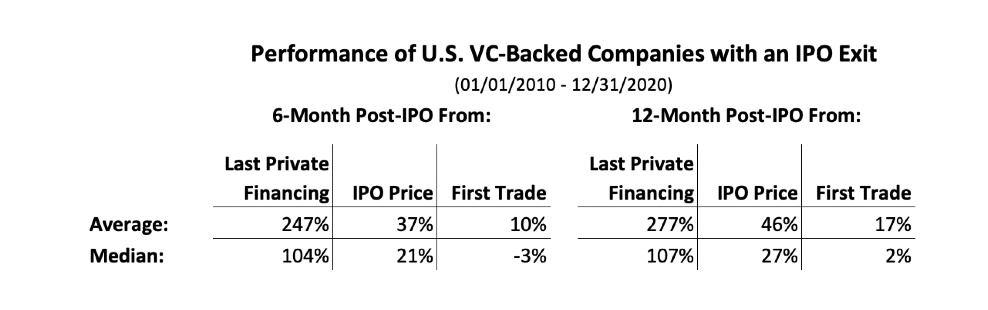

The following analysis shows that investors who were able to invest in the last private financings of venture capital (VC)-backed companies that went public over the last decade would have significantly outperformed investors who waited to access these companies at the IPO price or first trade.

Figure 1: U.S. VC-Backed IPO Analysis4

Source: SharesPost 100 Fund, Pitchbook, Y-Charts, Nasdaq, SEC Edgar. Total 557 U.S. Venture-Capital-Back Private Companies that executed an IPO from January 01, 2010 through December 31, 2020. Last private financing prices adjusted for subsequent stock splits to allow for appropriate comparisons. Only includes formerly VC-backed, U.S. companies listing on the NYSE or NASDAQ. Analysis tracks the change in price for an individual share at last private financing, and therefore does not factor in potential tax implications or management and performance fees that may be associated with investments in private markets.

In comparison to when Amazon went public over 20 years ago, a significant level of value appreciation is now happening in the private market before these companies go public simply by staying private for longer. Furthermore, staying private offers other attractive advantages, including:

- Minimizing disclosure requirements

- Avoiding complex and rigid securities regulations

- Maintaining more ownership and governance control

- Postponing the costs involved with entering and operating in public markets

- Prioritizing long-term strategic objectives over short-term quarterly public earnings guidance

The bottom line is that more companies are electing to remain private for much longer, which means that the bulk of their growth and value appreciation occurs outside of public markets. In addition, two-thirds of venture-backed companies have historically been acquired. This means they never even become available to public market investors.

By staying private for longer in a structurally illiquid asset class, there are potentially attractive inefficiencies that sophisticated private market investors may exploit due to the reality that underlying investors and shareholders in these companies often have different liquidity timelines.

Institutional Evolution of the Venture Capital Asset Class

While the late-stage venture capital asset class is only one part of the vast private market ecosystem, it may be one of the most promising areas for investment. During the past decade, according to the National Venture Capital Association, more than $1 trillion of the $6 trillion in private market asset flows have been allocated to venture capital, mostly late-stage assets.

Non-traditional asset sources such as sovereign wealth funds, mutual funds and hedge funds are increasingly directing capital towards this space. That’s because the sophisticated investors that run these vehicles recognize how much growth occurs in this stage of the corporate life cycle and believe there is less perceived risk than earlier stage companies, thus creating high demand.

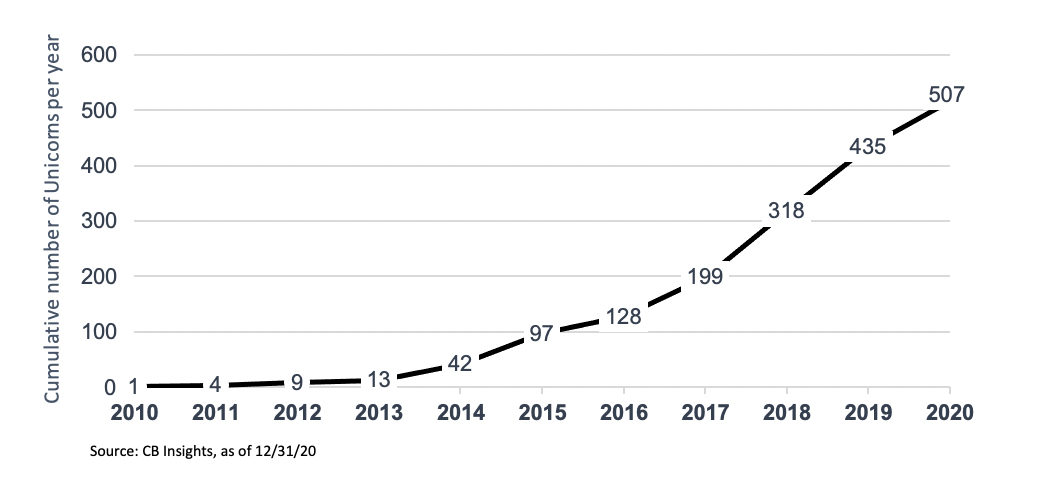

Within the late-stage venture capital category are private companies often called unicorns, a designation that implies an enterprise valuation of at least $1 billion. The growth of unicorns has surged over the last decade to more than 500 across the globe representing $1.8 trillion in aggregate enterprise value, which reveals the power and scope of this sector of the market.

Figure 2: Cumulative Number of Unicorns Has Increased Dramatically

Demand For Late-Stage Technology and Innovation

While there was a temporary slowdown in late-stage venture backed exit activity during the first half of 2020 due to COVID-19 related uncertainty, a surge in both traditional Initial Public Offerings (IPOs) and Special Purpose Acquisition Companies (SPACs) pushed the number and deal value of exits to record highs. Mergers and acquisitions (M&A) involving this asset class also remained resilient in 2020.

Exit activity involving late-stage venture backed companies has been steady over the past decade, and the record levels achieved in 2020 is a strong indication of heightened public market investor and strategic acquirer interest in technology and innovation-oriented private companies. Market experts anticipate this trend to continue, with no end in sight.

How To Access the Late-Stage Market

The historically attractive return profile of the late-stage venture market has typically only been available to institutional and high net worth investors that satisfy certain accreditation requirements and large minimum investment amounts. As a result, many investors and their advisors require democratization of investment vehicles to access this market opportunity. When these investors–and their advisors–are afforded the ability to allocate capital to this emerging asset class, Americans may have the opportunity to improve their prospects for investment growth beyond the public markets.

At Liberty Funds, our goal is to open up these markets to as many investors as possible. The SharesPost 100 Fund is a closed-end interval fund that offers individuals, family offices, and institutions an effective means to access the venture-backed asset class for a minimum investment of $2,500 and without investor accreditation requirements.

About Christian Munafo

Christian Munafo is the chief investment officer of Liberty Street Funds and the portfolio manager of the SharesPost 100 Fund. Mr. Munafo has 20 years of experience in finance, with the last 15 years focused on secondary investments involving venture-backed and growth equity-oriented companies and funds. During this time, he has also served on the boards of many of these companies and funds. Previously, Christian was Co-Head of the Global Private Equity Secondaries Practice at HQ Capital based in New York. Prior to that, he served as Head of Secondaries at Thomas Weisel Partners. In aggregate, Christian has helped raise more than $1 billion globally from institutional investors, corporations, pensions, endowments and family offices, and has completed or overseen the completion of more than 100 secondary transactions representing over $1 billion in capital commitments. Christian received his BA from Rutgers College.

About Liberty Street

The Liberty Street Funds offer investors and financial advisors mutual funds sub-advised by independent boutique managers who possess expertise in their asset class. Because Liberty Street focuses on boutique managers, financial advisors can provide value-added strategies in actively managed and less-correlated portfolios to their clients. Through its selective multi-manager family of funds, Liberty Street provides access to timely investment strategies. The Liberty Street Funds are based in New York City, NY and advised by Liberty Street Advisors, Inc. HRC Fund Associates, LLC, Member FINRA/SIPC, is an affiliate of Liberty Street.

For more information, financial professionals should contact their wholesaler by calling HRC Fund Associates, LLC. Advisors, Inc. at libertystreet@hrcfinancialgroup.com or 212-240-9726. Individual investors and shareholders should contact their financial advisor, or the Fund at 800-207-7108.

Important Disclosure

As of December 9, 2020, Liberty Street Advisors, Inc. became the adviser to the Fund. The Fund’s portfolio managers did not change. Effective April 30, 2021, the Fund changed its name from the “SharesPost 100 Fund” to “The Private Shares Fund.” Effective July 7, 2021, the Fund made changes to its investment strategy. In addition to directly investing in private companies, the Fund may also invest in private investments in public equity (“PIPEs”) where the issuer is a special purpose acquisition company (“SPAC”), and profit sharing agreements.

Investors should consider the investment objectives, risks, charges and expenses carefully before investing. For a prospectus with this and other information about The Private Shares Fund (the "Fund"), please download here, or call 1-855-551-5510. Read the prospectus carefully before investing.

The investment minimums are $2,500 for the Class A Share and Class L Share, and $1,000,000 for the Institutional Share

Investment in the Fund involves substantial risk. The Fund is not suitable for investors who cannot bear the risk of loss of all or part of their investment. The Fund is appropriate only for investors who can tolerate a high degree of risk and do not require a liquid investment. The Fund has no history of public trading and investors should not expect to sell shares other than through the Fund's repurchase policy regardless of how the Fund performs. The Fund does not intend to list its shares on any exchange and does not expect a secondary market to develop.

All investing involves risk including the possible loss of principal. Shares in the Fund are highly illiquid, and can be sold by shareholders only in the quarterly repurchase program of the Fund which allows for up to 5% of the Fund's outstanding shares at NAV to be redeemed each quarter. Due to transfer restrictions and the illiquid nature of the Fund's investments, you may not be able to sell your shares when, or in the amount that, you desire. The Fund intends to primarily invest in securities of private, late-stage, venture-backed growth companies. There are significant potential risks relating to investing in such securities. Because most of the securities in which the Fund invests are not publicly traded, the Fund's investments will be valued by Liberty Street Advisors, Inc. (the "Investment Adviser") pursuant to fair valuation procedures and methodologies adopted by the Board of Trustees. While the Fund and the Investment Adviser will use good faith efforts to determine the fair value of the Fund's securities, value will be based on the parameters set forth by the prospectus. As a consequence, the value of the securities, and therefore the Fund's Net Asset Value (NAV), may vary.

There are significant potential risks associated with investing in venture capital and private equity-backed companies with complex capital structures. The Fund focuses its investments in a limited number of securities, which could subject it to greater risk than that of a larger, more varied portfolio. There is a greater focus in technology securities that could adversely affect the Fund’s performance. The Fund's quarterly repurchase policy may require the Fund to liquidate portfolio holdings earlier than the Investment Adviser would otherwise do so and may also result in an increase in the Fund's expense ratio. Portfolio holdings of private companies that become publicly traded likely will be subject to more volatile market fluctuations than when private, and the Fund may not be able to sell shares at favorable prices, such companies frequently impose lock-ups that would prohibit the Fund from selling shares for a period of time after an initial public offering (IPO). Market prices of public securities held by the Fund may decline substantially before the Investment Adviser is able to sell the securities.

The Fund may invest in private securities utilizing special purpose vehicles ("SPV"s), private investment funds (“Private Funds”), private investments in public equity ("PIPE") transactions where the issuer is a special purpose acquisition company ("SPAC"), and profit sharing agreements. The Fund will bear its pro-rata portion of expenses on investments in SPVs, Private Funds, or similar investment structures and will have no direct claim against underlying portfolio companies. PIPE transactions involve price risk, market risk, expense risk, and the Fund may not be able to sell the securities due to lock-ups or restrictions. Profit sharing agreements may expose the Fund to certain risks, including that the agreements could reduce the gain the Fund otherwise would have achieved on its investment, may be difficult to value and may result in contractual disputes. Certain conflicts of interest involving the Fund and its affiliates could impact the Fund’s investment returns and limit the flexibility of its investment policies. This is not a complete enumeration of the Fund's risks. Please read the Fund prospectus for other risk factors related to the Fund.

The Fund may not be suitable for all investors. Investors are encouraged to consult with appropriate financial professionals before considering an investment in the Fund.

Companies that may be referenced on this website are privately-held companies. Shares of these privately-held companies do not trade on any national securities exchange, and there is no guarantee that the shares of these companies will ever be traded on any national securities exchange.

The Private Shares Fund is distributed by FORESIDE FUND SERVICES, LLC

Private Shares Fund

Top 10 Holdings as of 12/31/2024*

*Represents 37.85% of Fund holdings as of December 31, 2024. Holdings are subject to change. Not a recommendation to buy, sell, or hold any particular security. Current and future holdings are subject to risk. To view the Fund’s complete holdings, visit privatesharesfund.com/portfolio.

Important Disclosure

As of December 9, 2020, Liberty Street Advisors, Inc. became the adviser to the Fund. The Fund’s portfolio managers did not change. Effective April 30, 2021, the Fund changed its name from the “SharesPost 100 Fund” to “The Private Shares Fund.” Effective July 7, 2021, the Fund made changes to its investment strategy. In addition to directly investing in private companies, the Fund may also invest in private investments in public equity (“PIPEs”) where the issuer is a special purpose acquisition company (“SPAC”), and profit sharing agreements.

Investors should consider the investment objectives, risks, charges and expenses carefully before investing. For a prospectus with this and other information about The Private Shares Fund (the "Fund"), please download here, or call 1-855-551-5510. Read the prospectus carefully before investing.

The investment minimums are $2,500 for the Class A Share and Class L Share, and $1,000,000 for the Institutional Share

Investment in the Fund involves substantial risk. The Fund is not suitable for investors who cannot bear the risk of loss of all or part of their investment. The Fund is appropriate only for investors who can tolerate a high degree of risk and do not require a liquid investment. The Fund has no history of public trading and investors should not expect to sell shares other than through the Fund's repurchase policy regardless of how the Fund performs. The Fund does not intend to list its shares on any exchange and does not expect a secondary market to develop.

All investing involves risk including the possible loss of principal. Shares in the Fund are highly illiquid, and can be sold by shareholders only in the quarterly repurchase program of the Fund which allows for up to 5% of the Fund's outstanding shares at NAV to be redeemed each quarter. Due to transfer restrictions and the illiquid nature of the Fund's investments, you may not be able to sell your shares when, or in the amount that, you desire. The Fund intends to primarily invest in securities of private, late-stage, venture-backed growth companies. There are significant potential risks relating to investing in such securities. Because most of the securities in which the Fund invests are not publicly traded, the Fund's investments will be valued by Liberty Street Advisors, Inc. (the "Investment Adviser") pursuant to fair valuation procedures and methodologies adopted by the Board of Trustees. While the Fund and the Investment Adviser will use good faith efforts to determine the fair value of the Fund's securities, value will be based on the parameters set forth by the prospectus. As a consequence, the value of the securities, and therefore the Fund's Net Asset Value (NAV), may vary.

There are significant potential risks associated with investing in venture capital and private equity-backed companies with complex capital structures. The Fund focuses its investments in a limited number of securities, which could subject it to greater risk than that of a larger, more varied portfolio. There is a greater focus in technology securities that could adversely affect the Fund’s performance. The Fund's quarterly repurchase policy may require the Fund to liquidate portfolio holdings earlier than the Investment Adviser would otherwise do so and may also result in an increase in the Fund's expense ratio. Portfolio holdings of private companies that become publicly traded likely will be subject to more volatile market fluctuations than when private, and the Fund may not be able to sell shares at favorable prices, such companies frequently impose lock-ups that would prohibit the Fund from selling shares for a period of time after an initial public offering (IPO). Market prices of public securities held by the Fund may decline substantially before the Investment Adviser is able to sell the securities.

The Fund may invest in private securities utilizing special purpose vehicles ("SPV"s), private investment funds (“Private Funds”), private investments in public equity ("PIPE") transactions where the issuer is a special purpose acquisition company ("SPAC"), and profit sharing agreements. The Fund will bear its pro-rata portion of expenses on investments in SPVs, Private Funds, or similar investment structures and will have no direct claim against underlying portfolio companies. PIPE transactions involve price risk, market risk, expense risk, and the Fund may not be able to sell the securities due to lock-ups or restrictions. Profit sharing agreements may expose the Fund to certain risks, including that the agreements could reduce the gain the Fund otherwise would have achieved on its investment, may be difficult to value and may result in contractual disputes. Certain conflicts of interest involving the Fund and its affiliates could impact the Fund’s investment returns and limit the flexibility of its investment policies. This is not a complete enumeration of the Fund's risks. Please read the Fund prospectus for other risk factors related to the Fund.

The Fund may not be suitable for all investors. Investors are encouraged to consult with appropriate financial professionals before considering an investment in the Fund.

Companies that may be referenced on this website are privately-held companies. Shares of these privately-held companies do not trade on any national securities exchange, and there is no guarantee that the shares of these companies will ever be traded on any national securities exchange.

The Private Shares Fund is distributed by FORESIDE FUND SERVICES, LLC